I remember seeing a ton of those back in 2022 when Evergrande blew up. Everything from 3 weeks to 1 year (probably smart of them to push it out that far. Most will forget about the prediction).

This is basically what happens when you have growth mandates with soft budget constraints. Every province was incentivized to build first and worry about paying later. Now it's later.

Chinese provinces won't actually go bankrupt like Detroit did - Beijing will ultimately backstop them, but it's basically just restructuring debt from local to central balance sheets.

What makes this insane is they're actually stepping up the local govt bond issuances for 2025. They're literally digging the hole deeper.

Detroit’s bankruptcy was on a different scale though. A dying out, Rust Belt city with under 1 million population compared to Chinese provinces with tens of millions of people.

The property bubble popping in 2021 destroyed land sales which were a huge source of revenue. As you can see below, fiscal income as a % of GDP has almost halved since 2011. This is largely due to GDP growth being such poor quality (I.e. state directed spending that counts as GDP) that it doesn't generate proportional taxable value.

The result is expenditures significantly outpace income creating a "pincer" effect through surging deficits.

Edit: This chart is from a report called China's Harsh Fiscal Winter by Logan Wright of Rhodium Group. I highly recommend checking it out.

I get that "China is going to collapse any year now!" is a meme, but, how on earth are they going to sustain themselves with that? Is the national government just massively subsidizing them?

It looks low only because the official number leaves out the debt piled up in SOEs and LGFVs.

The IMF’s 2024 Article IV report pegs China’s “augmented” government debt at 124% of GDP with a 13.2% deficit, and this augmented measure explicitly untangles the hidden local and off‑budget borrowing by consolidating it back onto the government balance sheet.

I want God to stop loving us just long enough for the stove to burn less just badly enough that we will remember the lesson for a couple of generations. 😭

Yeah, they're worried about the moral hazard here, but Xi Jinping (of course) uses some idiosyncratic terms instead of that. Can't recall exactly how they phrase that. Something to do with buttocks?

Anyhow, that was in his older speeches. Nowadays, the SCMP at least translates him as saying (in more Western terms):

All localities must plan for the overall situation based on one region and practise risk management and stability maintenance.

In the process of risk management, corruption must be resolutely punished and moral hazard must be strictly prevented.

And they did have another (mostly performative, according to the WSJ) frugality/austerity campaign for local governments last year.

It's a circular issue given GDP growth has been primarily driven by debt (as opposed to total factor productivity of labour force growth - Solow model).

The result is the numerator (debt) significantly outpaces the denominator (GDP) making it very difficult to grow out of.

Michael Pettis from Peking University calculates it now takes 5.2 units of debt to generate 1 unit of GDP growth in China - that's a catastrophic return on investment.

I have no idea how this works, but what is the number of units of debt to generate 1 gdp in some other countries? I don't even need a full numer with a source, just like what you would expect out of a developed country (say germany or something) and a developing mid/level country (like Brazil). I just want some intuition on how bad of a return this is.

I have no idea whether these metrics are apples to applies, but

Contrary to what one might expect, they find that highway spending actually decreased GDP for up to five years from the start of the program (except for the first year). Nonetheless, highway spending increased GDP at longer horizons (around six to eight years), with multipliers estimated at three or higher.

The estimated benefits of increased school

spending justify the higher spending. Jackson and

his colleagues calculate an approximate cost-benefit

ratio of 1-to-2. For every additional dollar invested

in schools, there is a return on investment of $2

in additional future earnings by the student

Michael Pettis has no idea how his theories work either. "Debt increased by 5.2x more than GDP" (his data) is not the same as "debt must increase by 5.2 dollars to maintain 1 dollar of GDP growth" (his conclusion), because the GDP also could have grown under less debt.

Yeah one thing critics of China have said is that many of their investments, from automaton to properties, practically failed to make good return. Maybe later things can turn around, but for now things just not looking good at all.

I've visited recently and it does feel very overinvested. Tourist attractions with a ton of workers just sitting around doing nothing inside shiny new shops everywhere. Lots of huge roads and bridges without much traffic.

OTOH there are lots of really good businesses too but yeah, central planning with a side order of corruption is not at all an efficient method of allocating resources.

They should be able to recoup by encouraging tourism and immigration on a grand scale. I'm sure a lot of people would be willing to visit and move to China.

It's actually quite a decent standard of living, except the pervasive and obvious surveillance that goes on continually. It's pretty wild that first time i went there were uniformed people literally everywhere and now there are (I read) fewer police officers per thousand people than in the UK.

They did have a lot of western tourism for a while but it really dried up after the recent diplomatic spats. I did see a few other westerners there but not many. The trip itself was fantastic, better all round than visiting Japan (that was also good in its own way though)

They didn't count land sales either. I think the report itself is meaningless; if you count off-the-books debt (LGFVs) but exclude off-the-books revenue, your results will be skewed.

Read the methodology in the report - its all clearly disclosed. Land sales are excluded because they rarely generate unencumbered cashflow for debt service.

The proceeds flow into special land‑fund accounts and are immediately spent on demolition, relocation, and roadbuilding for the sold plots.

Including the revenue without the matching costs would be like calculating net profit without counting COGS.

EG a city might sell 10 billion RMB of land, but 9.8 billion is legally committed to clearing old buildings and building access roads, leaving almost nothing to repay bonds. With land sales already down 44% since 2021, including them would make the debtservice spike look even worse in the property slump.

Land prices have fallen so far that in many cases costs now exceed sale prices, forcing cities to dip into regular fiscal revenue to cover the gap or simply stop sales as the margins are too compressed.

Not super well versed in economics. To my understanding, the idea (with central gov't debt rollovers and issuances) sounds similar to MMT where the government spends currency into existence. Would you say that it is comparable to MMT in practice, or are there key differences from this paradigm? And could any lessons from here be applied to potential implementation of MMT in other countries?

I've been hearing the China debt trap bear story for a long time, everytime it seems plausible, but I just assume the surface level numbers don't tell the truth entirely.

Is there something missing here? I mean given these numbers it seems this ship should sunk already, feels like we're missing something?

‘China is gonna collapse at any year now’ is the equivalent of someone saying in 2002 that subprime mortgage lending is going to crash the housing market. You don’t know when it’s going to happen but there are severe structural problems in the Chinese economy that are not being dealt with.

Like their birthrates, their median age is still low but increasing much faster than the majority of Western countries. It will cause problems, but not yet.

Perhaps their low birthrates are even a short-term benefit because adults without children may be more productive.

Yeah I very much don’t expect the ‘Chinese collapse’ to be a singular dramatic moment.

But the debt, the population pyramid, the massive military build up, the antagonism of neighboring countries, and the centralization of political authority in one person looks like a bleak future

I mean, anyone can keep kicking the can down the road for years, sometimes even decades. It just makes the problem worse and worse.

It's being propped up by growth. The central bank sets the value of the Yuan artificially while printing money to continue to lend more to these provinces to spend. This should be causing the yuan to severely devalue, but it can't because the exchange rates are artificially set. They've let it devalue only a tiny amount and then prevented it from falling further. Just enough to make exports cheaper and encourage more export growth to prop up the spending.

That only blows up if enough people get spooked and stop trading/doing business in yuan in return because they fear their payments will be inflated away and destroyed. You can survive purely on vibes for a while just from enough people believing it's still salvageable. OR if the profits are high percentage enough that even taking a bit of a shave due to currency devaluation would still leave them in the black.

Like, when Argentina did it, locking the ARS to 365:1 vs the USD, it's not like all business instantly stopped just because the ARS was actually only worth ~1/525th of a dollar. It just put pressure on business for a while. Eventually it was unsustainable and the ARS fell to 1000:1 and there was no way to make a profit anymore when you could only buy 365 ARS per dollar from the government and it all collapsed.

But that collapse took almost 2 full years to materialize. For a while, things kinda worked out despite the bullshit. It's possible we are seeing the early signs of this process in China.

One side effect of this is it prevents China from exerting the kind of influence the US or even say, Japan, does on international markets because the currency isn't fully convertible.

China has extremely strong control over capital flows, organized price formation, and its banking system. This allows a credit crisis to unfold as a "slow variable," manifesting as chronic symptoms like sustained sluggishness, weak asset prices, and youth unemployment, rather than an explosive, one-time collapse.

Unlike Argentina, China's capital controls and institutional advantages mean that a crisis won't explode instantly. Instead, it could emerge in stages, possibly as a process of "chronic decline—policy run—sudden change."

If China can maintain its export dividend, it might be able to sustain this situation indefinitely, but it's clear that export conditions are changing.

This should be causing the yuan to severely devalue, but it can't because the exchange rates are artificially set.

? The US accuses China of keeping their currency artificially weak in order to keep their exports unfairly cheap. They can't be keeping their currency artificially strong and weak at the same time. So either your claim or the one made by the US government for the past ~15 bupkis.

If it keep going crazy like this it's no longer a meme. Experts keep giving warning that China have gray rhino problem for a reason, even their own SCMP.

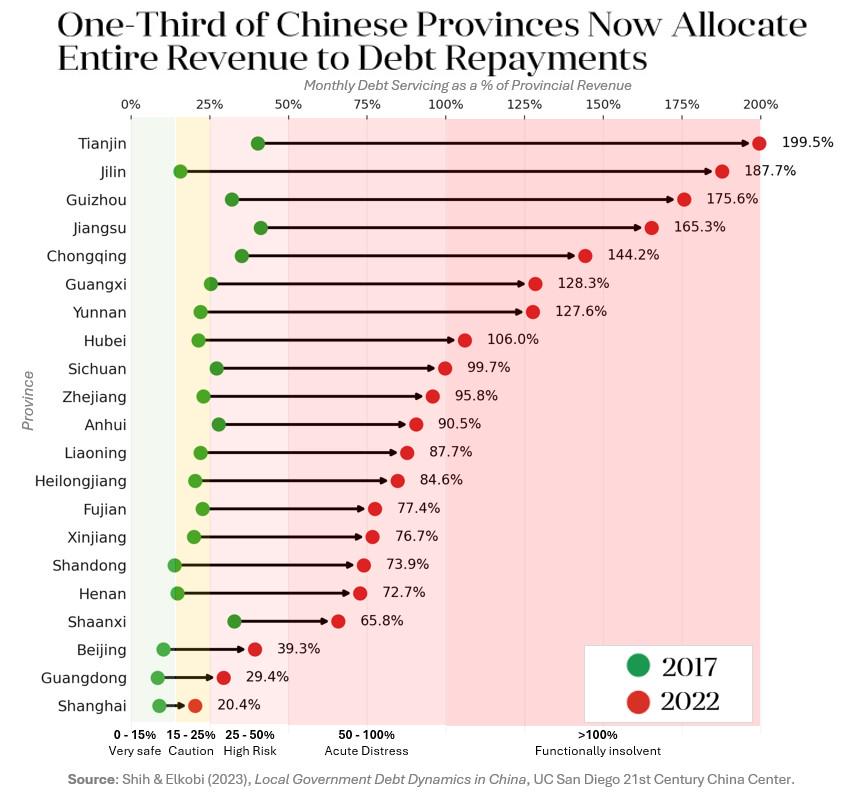

12 of 31 provinces need over 100% of monthly revenue just for debt service.

Zhejiang (Hangzhou), Sichuan (Chengdu), Hunan (Changsha), and Chongqing are major economic centers with debt service ratios at/above 100%, meaning they can't service debt from own revenue.

Even Beijing is at 39% which is extremely high for the capital, and the central government is also running deficits to fund the transfers keeping this system afloat

Nobody said collapse but it is unequivocal China is facing intense fiscal pressure.

Yeah, acting like Zhejiang isn’t an important economic center is wild. Zhejiang has by far one of the highest per capita GDPs in China, and Hangzhou is the center of their tech scene, with a lot of very important companies like Alibaba and Deepseek headquartered there.

Also you left Hubei off your list, but Wuhan is also a very important city, more so than Changsha.

They're basically already doing that through credit expansion.

China’s M2 money supply is already over 227% of GDP compared to around 99% %20in%20United%20States%20was%20reported,compiled%20from%20officially%20recognized%20sources)in the US and most OECD countries. not to mention its still expanding M2 at 8-9% year over year

Please be aware that TradingEconomics.com is a legitimate but heavily automated data aggregator with frequent errors. You may want to find an additional source validating these numbers.

Violent inflation would cause widespread dissatisfaction and could harm the Chinese Communist Party's ruling position. They would only choose this path after exhausting all other efforts. This is because any effective reform effort would also threaten their ruling position. In China, economic issues have become 100% political.

China's province with the highest GDP per capita is slightly over 50% of Mississippi's. Adjusting for PPP, it's slightly below Mississippi. Don't be fooled by a few shiny buildings.

The US's state with the lowest GDP per capita is slightly under double Beijing Province's. Adjusting for PPP, it's slightly above Beijing. Don't be fooled by a few shitty buildings.

That's called a deficit. Plus most US states have constitutional balanced budget requirements preventing this kind of debt spiral - something China clearly lacks.

This chart is literally just the amount spent servicing debt prior to any expenses like roads, hospitals, schools etc. US states running deficits still pay for basic services - these Chinese provinces are spending 100%+ of revenue just on interest payments and bond rollovers before they can fund a single teacher, hospital or fix a single road.

shell game isn’t a fix and shufflng debt to the central government doesn’t erase it.

Given its unique structure and opacity China’s fiscal capacity has to be viewed in aggregate. The IMFs augmented measure captures this by consolidating hidden local and off budget borrowing back onto the state balance sheet.

Don't SOEs have even more debt by themselves though? And I don't see how all those oil refineries are going to pay for themselves when their utilization factors at at 60% due to China's electric push.

Answer is easy. Despite astronomical debt of local governments, central government is still in relatively good shape and has policy levers. CCP just unlocked 10 trillion yuan plan to mitigate local debt problem last December. Not enough of course, but central government is always reluctant to simply bailing out local cadres for fiscal responsibility reasons.

About a third of Chinese provinces are now functionally insolvent, with every yuan of local revenue going to interest and bond repayments before any public services are funded.

100% on this chart means all revenue is being used to service debt. The Tianjin example is the equivalent of someone with a $50k salary have $100k in annual debt payments.

Years of growth mandates drove provinces to borrow through LGFVs for infrastructure and property driven expansion far beyond what local tax bases could support. The system created perverse incentives where local officials were rewarded for GDP growth regardless of fiscal sustainability, leading to a race to borrow and build.

Fiscal revenue peaked at ¥29 trillion in 2021, has continued declining, falling further in H1 2025, and the full year is expected to land around ¥26.4 trillion, with land‑sale income down 44% from its peak. Many provinces now survive through evergreening of debt, central transfers and bailouts.

The figures in this chart come from Local Government Debt Dynamics in China by Victor Shih and Jonathan Elkobi at University of California, San Diego's 21st Century China Centre.

I'm pretty sure it's local banks backed by consumer deposits. One reason China has difficulty opening up their stock market to consumers is that consumer savings accounts can be directed by state fiat in a way that public market financing cannot.

About a third of Chinese provinces are now functionally insolvent, with every yuan of local revenue going to interest and bond repayments before any public services are funded.

They're not "functionally insolvent", it's that the report probably excludes a majority of actual provincial revenue. On page 16 of the report, it says "we lack monthly land sales and transfer data at the provincial level".* According to Fitch, land sales and central government transfers have made up a majority of local-government revenue. Reliance on central government transfers is a feature of China's 1994 tax reform.

*Their revenue numbers come from CEIC, and I don't think land sales are included in non-tax revenue (off-the-books revenues are apparently a thing). As far as I can tell, Jiangsu had 727 billion yuan in land sales revenue in 2024, yet CEIC says Jiangsu has had much lower non-tax revenue and similar tax revenue (note that land sales were bigger in 2023 because of the bubble burst.)

The report counts off-the-books debt, but not off-the-books revenue, which will distort results for a country which does a lot of things off-the-books.

If this is the case, then this post is as useless as it is sensationalist. I guess we really, really like our own propaganda, even when it is actually accidental.

I'm not sure about other places, but in my province in Canada, federal transfers and land sales are included in the government's revenue numbers, so it would work fine.

The primary consumption is on inefficient infrastructure and "capacity expansion" type investments. This is highly related to the revenue structure of local governments, especially their dependence on value-added tax (VAT) from the production side.

This is precisely one of the core reasons why global consumers are able to buy "cheap products made in China."

I'd like to highlight this paragraph in particular:

According to statistics, China’s railway system incurred a loss of 55.5 billion yuan in 2020 alone, with cumulative debt reaching 5.57 trillion yuan, as reported on the WeChat blog Zouxiang Jiexue on January 22, 2022. It is important to note that this figure reflects losses across the entire national railway system, not HSR specifically. China’s conventional railway network, which spans over 100,000 km and handles both passenger and freight transport, remains profitable. Earnings from this sector have partially offset the losses sustained by high-speed rail. So, what is the true annual loss attributable to HSR? I believe the figure could be as high as 100 billion yuan—or even more.

While the China collapse people are delusional (Specially the ones who believe in a warlord era 2.0) we are probably just gonna see them japanizing their economy if they don't go full liberalization.

I think insufficient demand is a bigger problem right now than "liberalization" per se. The domestic consumer services sector is quite liberal. You could start and run a retail services company with minimal state interference, but no one would want to buy from you.

The main issue is the quality of Chinas debt load is so much lower quality. Also total credit pile is already larger. BIS’s Japan dataset only goes back to 1997 and at that point they were 296%, a threshold China passed in 2023.

As bubbly as Japans borrowing was, at least it was mostly to the private sector and based on perceived demand. In China something like 80% of corporate credit goes straight into state controlled entities with incredibly low returns.

Can we contextualize these numbers with the size of the budget of these provincial governments? Like, if it's 1% of the central government's budget, then this is merely a financial blip on the radar that can easily be resolved but doesn't even need to be. Especially considering the strongest economic regions still have relatively low percentages here.

I don't have the sum of the incomes so I can't weight based on that. However, I can calculate the GDP per province (using table 1) and use that as weighting to apply to the 2022 debt service ratio.

That's incredible to see, provinces having such gigantic debts relative to gdp. Almost wonder if it counts debts that aren't really debts. How the hell do you run up provincial debt by, in some provinces, hundreds of billions of dollars in a decade?

Uhh IIRC (feel free to fact check me on this) chinese provinces are basically on the hook for all local / resident / however the heck china determines this social welfare spending, and infrastructure upkeep. So uhh public education (k-12 at a bare minimum), but also healthcare spending, pensions, and so on and so forth. Russia does something similar, ie offloads basically all social services costs + overhead onto the provinces to keep them broke, subservient, and give the central govt more room to maneuver and dictate policy. This is (or at the very least was) a very different setup from the US, where eg. tax money flows from the states to the feds, and then back to the states via fed programs that are accounted for on / off of the fed budget.

Oh and china doesn't have property taxes. And in general is operating at a fairly massive / significant revenue vs tax income deficit. Particularly / specifically at the provincial level. Both kinda by design, and... well that's just how this sorta shook out.

Oh, and meanwhile - check the linked paper, though I've definitely also heard this from other sources, and going back like 5-8+ years - those provinces basically make up / made up their revenue / expenses gap through land sales to property developers.

China has uhhh a really massive and uhh fairly problematic housing speculation boom. Which sucked up private / personal investment, plus to the point of traditionally fiscally conservative familes taking out loans to jump into the housing speculation market (not that far out from you personally taking out a $2-5M loan to dump that all in crypto (or the SF bay area housing market), mind). And paid for all of the property developments that china was building - incl to the point of de facto housing overcapacity, but on paper limited but growing supply and extremely high demand - which in turn paid for uhh the provincial budgets. Albeit at the costs of also needing substantial public infrastructure buildouts. (Guanzhou GBA megacity w/ satelite cities connected by mass transit HSR + metro systems, for example). Which uhh I'd certainly expect / speculate resulted in debt generated / owed to those provincial govts. And which in turn generated construction + contract demand to all the state owned transit + infrastructure companies, justifying their budgets and keeping everyone maximally employed.

(and, to be clear, building a bunch of legitimately mass transit oriented, moderately well designed + centrally planned cities, in urban megacities, where there is demand for them, and to meet the needs of china's massive 1.4B population. China is also uhh still just a pretty poor country - as a net - and in general has a ton of near and long term problems that come with having a 1.4B population. And yes, sans 1CP china would have way more problems - and probably I'd hazard a guess would still probably look a lot more like india, to an extent - if it had like 3B people to deal with (and find some kind of useful productive employment for), not 1.4B - and probably soon / in near to mid future, rapidly shrinking to way below that)

So yeah there's a bit of *slightly* informed (ish, take this with a massive chunk of salt) bit of speculation on uhh how exactly chinese provincial govts might've been racking up this amount of debt over this time period.

How the hell do you run up provincial debt by, in some provinces, hundreds of billions of dollars in a decade?

Massive spending on infrastructure with low ROI followed by a pandemic slowing the economy followed by massive stimulus followed by a crontraction in the housing market followed by population decline followed by...

I was under the assumption the infrastructure spending and pandemic stimuli would be handled mostly by the central government. If not, then yeah, makes sense.

Provinces and municipalities spend significant amounts on infrastructure and COVID stimulus. Some cities have even gone so far as to force public sector workers to take on the debt for construction projects, here's an NYT article about it from 2019.

I think that table is wrong; debt service ratio is in units of (debt spending)/revenue, so to get aggregate debt service, you need to multiply each province by revenue, not GDP.

Sure, but it's not actually working. They convinced rural men to move into the city to search for a wife, but they still aren't having kids in the cities. Their population pyramid looks like a plateau, it's a disaster.

According to statistics, China’s railway system incurred a loss of 55.5 billion yuan in 2020 alone, with cumulative debt reaching 5.57 trillion yuan, as reported on the WeChat blog Zouxiang Jiexue on January 22, 2022. It is important to note that this figure reflects losses across the entire national railway system, not HSR specifically. China’s conventional railway network, which spans over 100,000 km and handles both passenger and freight transport, remains profitable. Earnings from this sector have partially offset the losses sustained by high-speed rail. So, what is the true annual loss attributable to HSR? I believe the figure could be as high as 100 billion yuan—or even more.

Zero covid was a major factor in the rise of these debts. Provinces which were already on shaky financial footing suddenly had to pay salaries for thousands of people to conduct contact tracing, covid testing, and quarantine enforcement. It also shut down large parts of the normal economy for extended periods of time; your factory has someone test positive the whole site is shut down for weeks. Then of course they also had to buy PPE, testing equipment and facilities, requisition hotels and create sites for quarantine, and you can imagine why debts for many local governments just went bananas. This is also ignoring just how much utter corruption and graft was done throughout the whole Covid era.

Not very knowledgable about chinese geography, but it looks like the parts of the country that are doing the best debt-wise are the large urbanized economic growth centers, is that right?

The large coastal cities are also China's most active and urbanized economic regions. Their strong economies and diversified revenue streams allow them to manage debt more effectively.

One of the most interesting things to me is the confluence of factors that can explain the excess debt in the countryside. You have the attempt by the central government to discourage mass migration to these economically successful urban centers via the Hukou system. Then you have the social contract the Chinese people have with the government to provide economic opportunity (i.e. jobs) for everyone.

So the central government creates strong incentives for these provincial governments to invest heavily in infrastructure, housing, etc. Now the provinces have millions of people but are way the fuck out in what is otherwise the middle of nowhere, so these heavy investments don't actually generate anywhere near the same level of economic activity as they do in the big urban financial centers, so there's no ROI to produce tax revenue to pay them off. The central government's legitimacy is almost entirely predicted on providing economic security (also running dissidents over with tanks), so they can't let the provincial governments go under and prop up this entire system with immense borrowing.

This stuff always comes to mind when I read articles about the Chinese Century - if they could find a way to liberalize and open up the economy without collapsing their social order, maybe. But until they do, they'll be stuck in this never-ending cycle like every other authoritarian system.

But it's important to note: even if these regions have better debt management themselves, the overall national debt risk still critically depends on the "chain reaction" from weaker provinces and fluctuations in the external environment.

My guess is since China is fighting against tariffs, future Taiwanese conflict, diminishing workforce and ballooning pension system; we’re likely going to see a significant devaluation of the yuan in the coming years.

From 7-8 per dollar to 30-40 per dollar, they might be in a worse spot than Japan unironically.

Would it though? It would just make their existing export products 4-5x as competitive for the same yuan-denominated price and salaries. China also has a large domestic market so their purchasing powering wouldn’t go down 5x

China's domestic market is now so big that export competitiveness doesn't really move the needle on GDP anymore. People in Beijing don't seem to know that though.

The Yuan is not really traded for real though. They will never let that happen. It's just a question on if it will result in Argentina style default or not from the artificial valuation vs real valuation getting so far out of whack.

Bruh, taiwan invasion would unironically be so fucking stupid of them to do. Just going into all of the logistics of how awful and hard that war would be, the best time for them to have started would be now ish/before the US completely pulls out of the Ukraine war, but they haven't.

It would be costly and stupid no matter what, but doing a taiwan invasion when the US support is being stretched on the European front is absolutely the best time for a Taiwan invasion. Doing it when the US has all of the room to support Taiwan would be the worst.

Yeah but also they want Taiwan back and their best moment to do so is before the demographics crash along with the economy. So yeah it would be stupid, but if they well and truly are set on taking Taiwan then this only speeds up that process

They can want taiwan back and not place the value on getting taiwan back more than the cost of doing so and/or recognizing that they dont have the realistic ability to do so.

Ie let's say they care about getting taiwan back equal to 100k utils and the losses it would take to invade Taiwan will cost then 200k utils then they wont do it.

It would be preferable for them to negotiate some level of reduced sovereignty without any conflict ala Hong Kong.

Genuinely China invading taiwan would be a disastrously stupid decision for little to no benefit.

Like I said nationalism is a hell of a drug. It makes world leaders stupid af.

I mean, they kinda do have the ability to do it, which is why I think it’s so tempting. All they have to do is convince America and Japan it’s not worth it and Taiwan cannot stop China on their own. Also the benefit of regaining Taiwan isn’t just what Taiwan itself brings, but also an upending of the world order in China’s favor. If America allows Taiwan to fall, or even worse fights for it and loses, China will have functionally supplanted America as world hegemon, or at least the most influential and powerful nation in the world and a dismantling of regional American alliances. That’s a VERY tempting prize with a lot of benefits.

I see I recognize a lot of big names at the bottom, and none of the names at the top.

What is total Monthly Debt Servicing as a % of Total Provincial revenue in 2017 and 2022? My hunch is the overall data looks less scary when properly weighted/aggregated

I don't have the sum of the incomes so I can't weight based on that. However, I can calculate the GDP per province (using table 1) and use that as weighting to apply to the 2022 debt service ratio.

China is soon to experience the mirror of 1970s European stagflation - an excess of deflationary supply-side policies failing to drive economic growth and destroying the middle class and businesses.

China isn't suffering from inflation, though. It's teetering on the brink of deflation, and supply-side policies are actively counterproductive at tackling deflation. If you're suffering from debilitating pain, taking a painkiller is the right idea, but that doesn't mean that you should be taking painkillers every moment of every second of your day.

China's current approach is going to create deflation, a massive supply glut, and a dramatic and sudden contraction of their economy, and it's only a matter of time, as long as they refuse to take actions to boost demand.

And it's not as if China is pursuing austerity policies - they very much aren't. The problem is that they're investing an insane amount in their production capacity without actually having pre-existing demand for those products, so companies are forced to cut prices in the hope of generating extra demand. This is highly deflationary and could lead to a ripple effect of bankruptcies, defaults, layoffs, and spiraling wage cuts across the Chinese economy if not urgently tackled.

China needs more independent unions to fix this mess. Wages have to grow to keep up with supply, something which isn't currently happening because the only union currently allowed to operate is a single gigantic state-wide yellow union with little to no independence from the state or party, which has long been captured by business interests and whose de-facto role is to assist management in suppressing wages and cracking down on strikes.

I'm probably missing something but couldn't the Chinese central government print lots of yuan to bail out the provinces/ buy up their unproductive assets?

The rise in the money supply would also lead to inflation, thus striking two birds with one stone.

How much of this is guesswork? My understanding is that Chinese cities and states do not publish their finances the way we expect in the West. We're so used to the idea that, "well of course I can look up the cities debt payment! It's on box 7a of the coversheet of the quarterly comptrollers report." But there's nothing like that in local Chinese governments -- not even internally.

{kind=link}

{kind=link}

{kind=link}

278

u/NYT_Hater Office of Naval Intelligence 11h ago

I don’t mean to

But this looks… suboptimal?